How to Improve Your Credit Score

Your credit score—a three-digit number lenders use to help them decide how likely it is they’ll be repaid on time if they grant you a credit card or loan—is an important factor in your financial life. The higher your scores, the more likely you are to qualify for loans and credit cards at the most favorable terms, which will save you money.

If your credit history is not where you want it to be, you’re not alone. Improving your credit scores takes time, but the sooner you address the issues that might be dragging them down, the faster your credit scores will go up. You can increase your scores by taking several steps, like establishing a track record of paying bills on time and paying down debt.

How Credit Scores Are Calculated

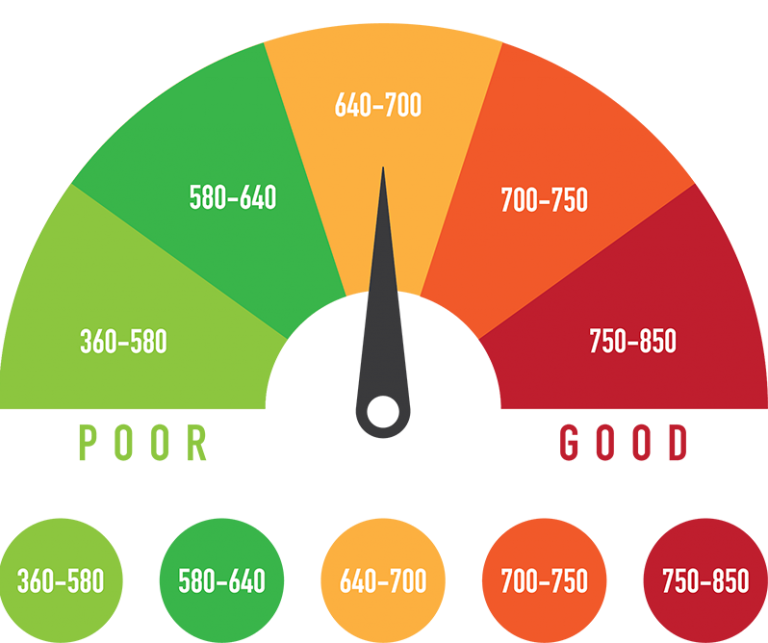

You likely have dozens, if not hundreds, of credit scores. That’s because a credit score is calculated by applying a mathematical algorithm to the information in one of your three credit reports, and there is no one uniform algorithm employed by all lenders or other financial companies to compute the scores. (Some credit scoring models are very common, like the FICO® Score* , which ranges from 300 to 850.)

You don’t have to get hung up on having multiple scores, though, because the factors that make your scores go up or down in different scoring models are usually similar.

Most scoring models take into account your payment history on loans and credit cards, how much revolving credit you regularly use, how long you’ve had accounts open, the types of accounts you have and how often you apply for new credit.

Steps to Improve Your Credit Scores

1. Pay Your Bills on Time

When lenders review your credit report and request a credit score for you, they’re very interested in how reliably you pay your bills. That’s because past payment performance is usually considered a good predictor of future performance.

You can positively influence this credit scoring factor by paying all your bills on time as agreed every month. Paying late or settling an account for less than what you originally agreed to pay can negatively affect credit scores.

You’ll want to pay all bills on time—not just credit card bills or any loans you may have, such as auto loans or student loans, but also your rent, utilities, phone bill and so on. It’s also a good idea to use resources and tools available to you, such as automatic payments or calendar reminders, to help ensure you pay on time every month.

If you’re behind on any payments, bring them current as soon as possible. Although late or missed payments appear as negative information on your credit report for seven years, their impact on your credit score declines over time: Older late payments have less effect than more recent ones.

2. Pay off Debt and Keep Balances Low on Credit Cards and Other Revolving Credit

The credit utilization ratio is another important number in credit score calculations. It is calculated by adding all your credit card balances at any given time and dividing that amount by your total credit limit. For example, if you typically charge about $2,000 each month and your total credit limit across all your cards is $10,000, your utilization ratio is 20%.

To figure out your average credit utilization ratio, look at all your credit card statements from the last 12 months. Add the statement balances for each month across all your cards and divide by 12. That’s how much credit you use on average each month.

Lenders typically like to see low ratios of 30% or less, and people with the best credit scores often have very low credit utilization ratios. A low credit utilization ratio tells lenders you haven’t maxed out your credit cards and likely know how to manage credit well. You can positively influence your credit utilization ratio by:

- Paying off debt and keeping credit card balances low.

- Becoming an authorized user on another person’s account (as long as they use credit responsibly).

3. Apply for and Open New Credit Accounts Only as Needed

Don’t open accounts just to have a better credit mix—it probably won’t improve your credit score.

Unnecessary credit can harm your credit score in multiple ways, from creating too many hard inquiries on your credit report to tempting you to overspend and accumulate debt.

4. Don’t Close Unused Credit Cards

Keeping unused credit cards open—as long as they’re not costing you money in annual fees—is a smart strategy, because closing an account may increase your credit utilization ratio. Owing the same amount but having fewer open accounts may lower your credit scores.

5. Don’t Apply for Too Much New Credit, Resulting in Multiple Inquiries

Opening a new credit card can increase your overall credit limit, but the act of applying for credit creates a hard inquiry on your credit report. Too many hard inquiries can negatively impact your credit score, though this effect will fade over time. Hard inquiries remain on your credit report for two years.

6. Dispute Any Inaccuracies on Your Credit Reports

You should check your credit reports at all three credit reporting bureaus (TransUnion, Equifax, and Experian, the publisher of this piece) for any inaccuracies. Incorrect information on your credit reports could drag your scores down. Verify that the accounts listed on your reports are correct. If you see errors, dispute the information and get it corrected right away.